16 May Managed SD-WAN Services Reality Check

May 16, 2019

More than one hundred SD-WAN products and services are available now – with more planned for launch this year. The term SD-WAN is being applied to nearly everything, including remodeled routers, WAN optimization and security equipment, appliance-based solutions, OTT service software, cloud-based offerings and integrated network-based services.

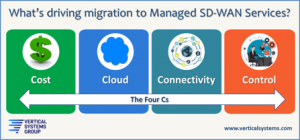

The focus of Vertical Systems Group’s SD-WAN research is Carrier Managed SD-WAN Services. These offerings address the rapidly changing networking requirements of enterprise and large business customers worldwide. What’s driving customer migration to SD-WAN services are the four interrelated Cs – Cost, Cloud, Connectivity and Control.

The focus of Vertical Systems Group’s SD-WAN research is Carrier Managed SD-WAN Services. These offerings address the rapidly changing networking requirements of enterprise and large business customers worldwide. What’s driving customer migration to SD-WAN services are the four interrelated Cs – Cost, Cloud, Connectivity and Control.

Managed VPN Segments: SD-WAN, MPLS and Site-to-Site

SD-WAN is one of the three Managed VPN segments that we track, along with MPLS and Site-to-Site VPNs. This segmentation is important. Our service migration analysis shows that the majority of billable Carrier Managed SD-WAN service installations are hybrid configurations that include partial conversions of existing Site-to-Site and MPLS networks.

SD-WAN, MPLS and Site-to-Site VPNs all enable secure transport of IP-based applications over network access connections between customer edge sites and data centers. However, there are significant differences when you compare these VPN service types based on functionality, service orchestration, underlying transport, access connectivity, application performance (e.g., latency, jitter, etc.), SLAs, cloud connectivity, network reliability, and recurring monthly costs.

SD-WAN, MPLS and Site-to-Site VPNs all enable secure transport of IP-based applications over network access connections between customer edge sites and data centers. However, there are significant differences when you compare these VPN service types based on functionality, service orchestration, underlying transport, access connectivity, application performance (e.g., latency, jitter, etc.), SLAs, cloud connectivity, network reliability, and recurring monthly costs.

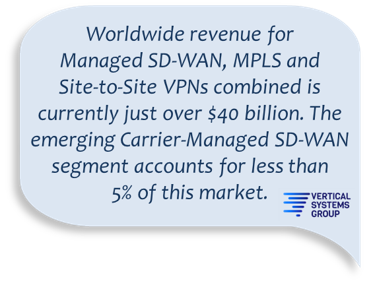

Market penetration for Managed VPN services also differs considerably based on Vertical’s latest research. Worldwide revenue for Managed SD-WAN, MPLS and Site-to-Site VPNs combined is currently just over $40 billion. The emerging Carrier-Managed SD-WAN segment accounts for less than 5% of this market.

Definition Challenges

Defining the Managed SD-WAN Services market is a challenge, due in part to the broad and growing number of vendor-proprietary SD-WAN products and service solutions. Results of the most recent MEF/Vertical survey of Service Providers worldwide measured the extent of this diversity. Delivery of managed SD-WAN services encompasses Hybrid SD-WAN solutions, multiple SD-WAN vendors, OTT solutions – and more. Additionally, in conjunction with their goals to virtualize and automate all network functions, many network operators are developing their own SDN-based solutions that integrate SD-WAN and other applications.

That is why 82% of Service Providers said that their most significant challenge for offering Managed SD-WAN Services is the lack of standardized interoperability between SD-WAN devices from different vendors. The lack of an industry-accepted SD-WAN definition was also cited as a major challenge.

MEF is responding to these industry needs with MEF 70, the first standard for SD-WAN services. As an integral component of the MEF 3.0 Framework, MEF 70 defines a common terminology for buying, selling, assessing, deploying, and delivering SD-WAN services.

What is a Carrier Managed SD-WAN Service?

Vertical Systems Group’s definition for a Carrier Managed SD-WAN Service and its required components and functionality is described below. It aligns with MEF terminology for an SD-WAN service.

CARRIER MANAGED SD-WAN SERVICE DEFINITION

Required Components and Functionality

Service Based on SDN Architecture

- Carrier-grade network service for business customers that is managed by a network operator

- Service architecture uses Software Defined Network (SDN) technology with independent management of the control and data planes

- Centralized SD-WAN Service Orchestrator/Controller provides orchestration, management and application visibility to all SD-WAN sites

- Customer edge sites (i.e., Branch, HQ, Data Center, etc.) have either a purpose-built SD-WAN appliance or a CPE-hosted SD-WAN VNF (Virtual Network Function)

- An SD-WAN UNI (User Network Interface) at each customer site is the demarcation between the responsibility of the network operator and the customer

Dynamic Customer Edge Site Connectivity

- Creates and terminates multiple secure virtual tunnels over an SD-WAN UNI

- Capable of supporting two or more active underlay connectivity services (i.e., WAN Access connections) at each customer site

- Supports dynamic multi-path, multi-link optimization of traffic flows end-to-end based on application and network performance policies

- Automated failover that is fast enough to maintain all active sessions in response to connectivity loss or service degradation

Centralized Network Control and Visibility

- Real-time monitoring and end-to-end visibility of network and application performance via a User Web Portal or APIs

- Supports scheduled, on-demand or automated changes to connection parameters and application policies

Security and cloud connect are two other capabilities that SD-WAN customers typically require. Security (i.e., firewall, malware protection, etc.) is most essential, and may be integral to the SD-WAN service. Cloud connect facilitates direct, secure connectivity to private or public clouds (e.g., to AWS, Azure, etc.).

Not considered Carrier Managed SD-WAN Services: DIY (Do It Yourself) SD-WAN solutions purchased from an SD-WAN technology supplier, systems integrator, or Cloud provider.

Service Providers Worldwide & LEADERBOARD

Carrier Managed SD-WAN Services are available from the following companies (in alphabetical order): Aryaka, AT&T, Bigleaf, BT, CenturyLink, China Telecom, Colt, Comcast, Frontier, Fusion, GTT, Hughes, Masergy, Meriplex, MetTel, NTT, Optus, Orange Business, PCCW, SingTel, Spectrum Enterprise, Sprint, T-Systems, Tata, Telefonica, Telia, Telus, TPx, Verizon, Vertel, Vodafone, Windstream, Zayo and others throughout the world.

See Vertical’s first Carrier Managed SD-WAN Services LEADERBOARD here. This new benchmark ranks the top U.S. providers based on market share results for year-end 2018.

Reality Strikes

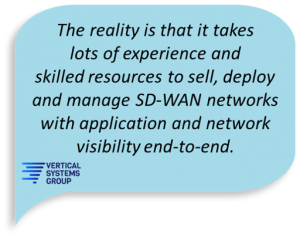

Misperceptions about SD-WAN have delayed network purchase decisions and limited market growth. Migration to SD-WAN is a more complex undertaking than has been pitched to date, particularly for larger enterprise and global networks. It requires managing a customer’s digital transformation, providing education about SD-WAN alternatives, setting customer expectations, and delivering a quality customer experience. The reality is that it takes lots of experience and skilled resources to sell, deploy and manage SD-WAN networks with application and network visibility end-to-end.

Misperceptions about SD-WAN have delayed network purchase decisions and limited market growth. Migration to SD-WAN is a more complex undertaking than has been pitched to date, particularly for larger enterprise and global networks. It requires managing a customer’s digital transformation, providing education about SD-WAN alternatives, setting customer expectations, and delivering a quality customer experience. The reality is that it takes lots of experience and skilled resources to sell, deploy and manage SD-WAN networks with application and network visibility end-to-end.

Rosemary Cochran is a Principal and Co-Founder of Vertical Systems Group.

@SD-WAN is available now exclusively by subscription to an ENS Research Program. Research topics cover the market share detail that powers the Carrier Managed SD-WAN Services LEADERBOARD, projected revenue, billable sites, customer counts, WAN Access connections, pricing by connection type (i.e., DIA, MPLS, Broadband, LTE/4G/5G, etc.), and site configurations (i.e., MPLS+DIA, BB+BB, etc.). Analysis includes SD-WAN migration drivers, profiles of top providers, technology status for top providers, plus Directories of Managed SD-WAN Services network operators and technology suppliers – and more.

Contact us to receive public LEADERBOARD releases or ENS Research Program subscription information and pricing.